EP 1: OVV Investor Relations

Hello, I’m Doug Shittles and I would like to review Ovintiv’s latest slide deck for you. This is how you *should* build an E&P IR deck.

Pretty pictures, high projected confidence and excessive patting on the back. Let’s dig in, shall we?

Slide 1:

The best part about the Montney is the views… if the wells don’t have economic type curves then we can at least show you trees.

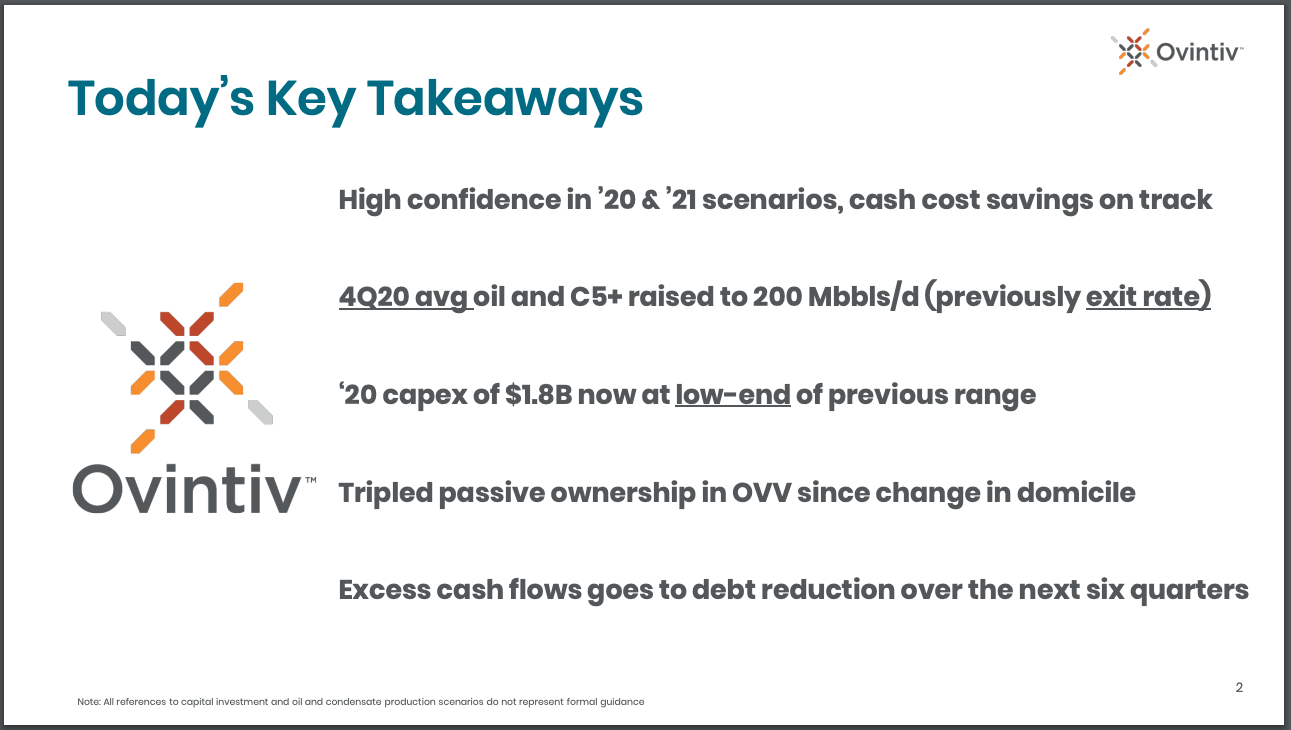

Slide 2:

There’s a lot to unpack here.

- If there isn’t high confidence in 2021 then I don’t want it!!

- Too bad that the tripling in ownership led to new investors being down 50+% YTD

- 2020 capex at the low end of the range? Look at us! The only thing we spend $$ on is our exec comp packages!

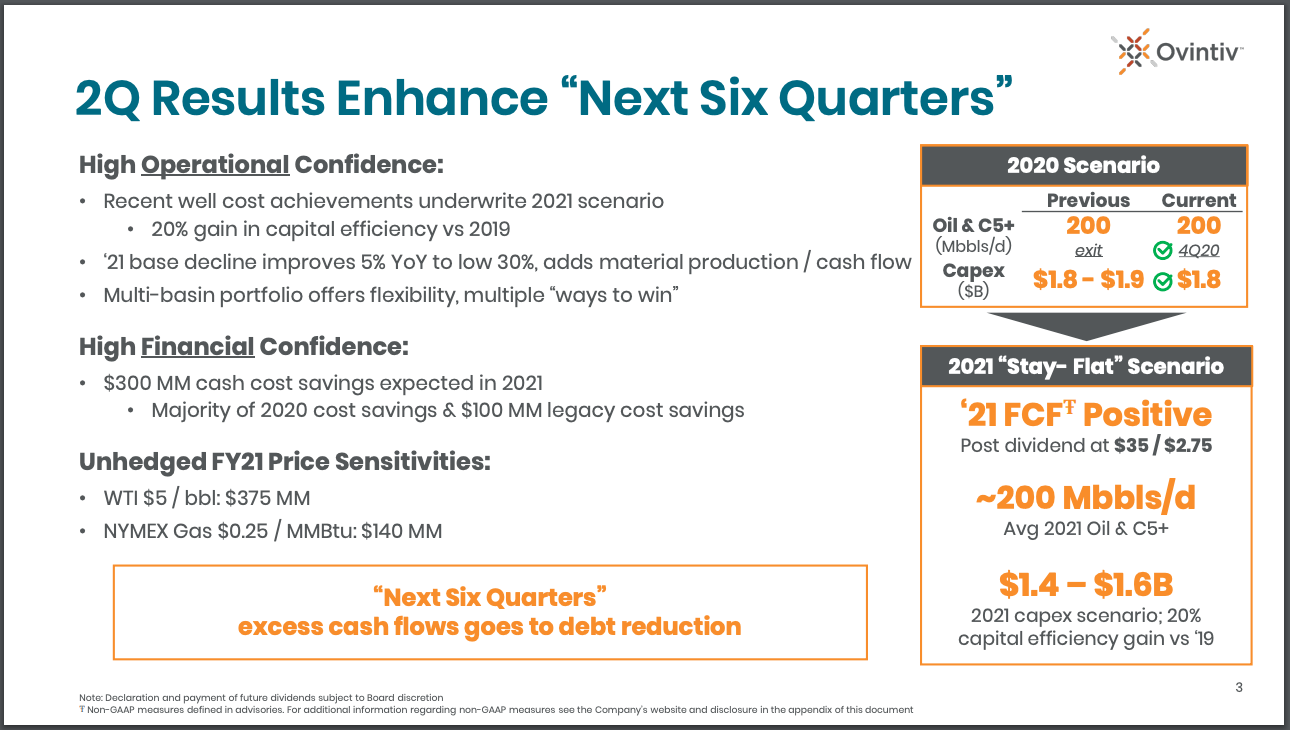

Slide 3:

- Why are the “Next Six Quarters” in quotes? That’s OVV’s shot clock until bankruptcy.

- See bullet point #1 on slide 2 – if we don’t have confidence then we don’t have anything but underperforming cube developments.

- How do we know that OVV’s base decline is low? They told us that 30% YOY decline is low! And we wouldn’t know that material production and cash flow is influenced otherwise.

Slide 4:

Top left figure looks a bit familiar…

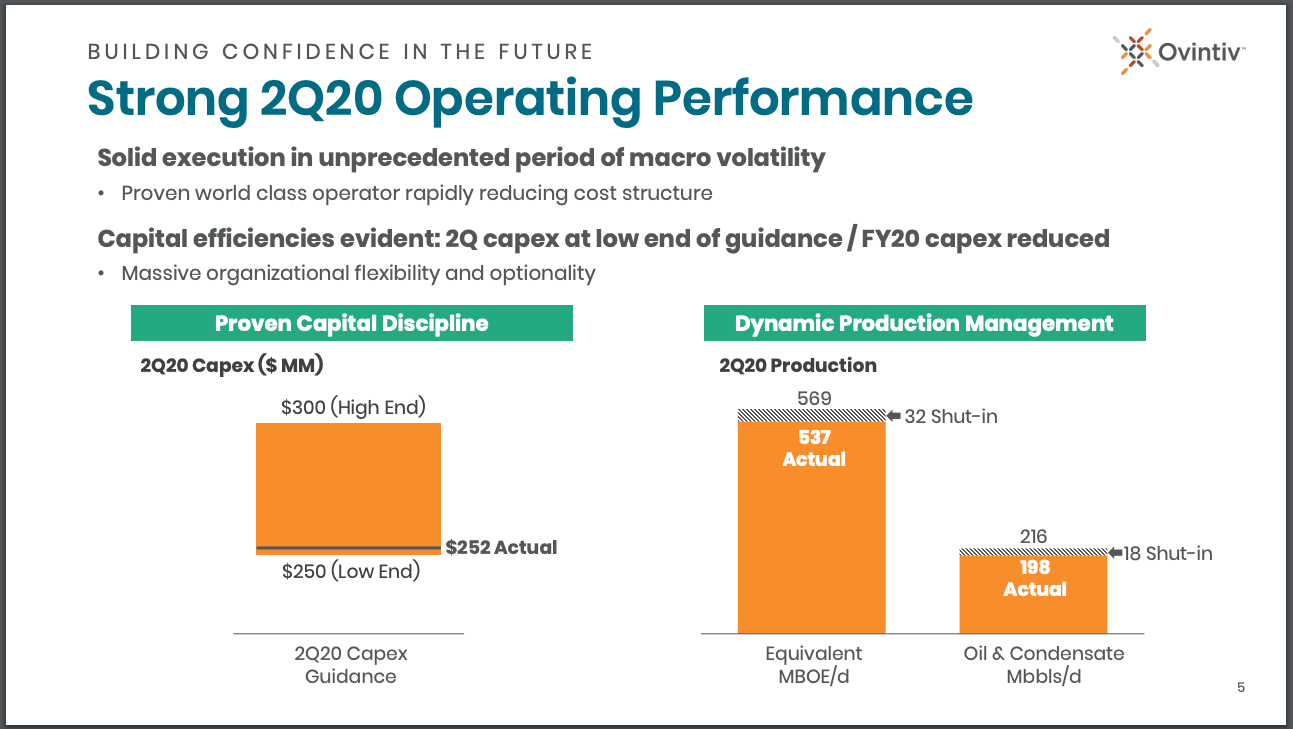

Slide 5:

You’re damn right that OVVs production management is dynamic… that’s how you know you’re a proven world-class operator™. Also dynamic is our BOE conversion – gotta adjust for ripping past the bubble point in all of our cubes.

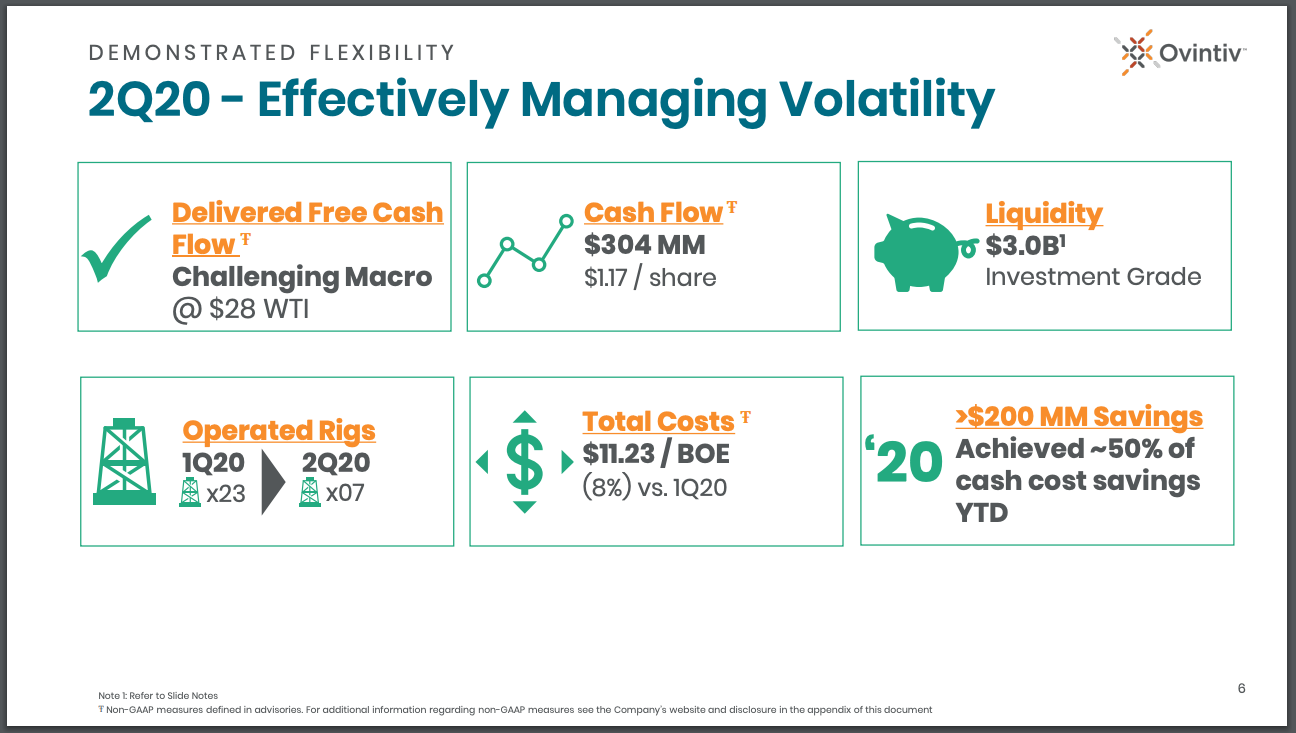

Slide 6:

When three of the six bullet points have an asterisk at the end to remind you about Non-GAAP advisories, you’ve really got a company you can trust. Buy OVV.

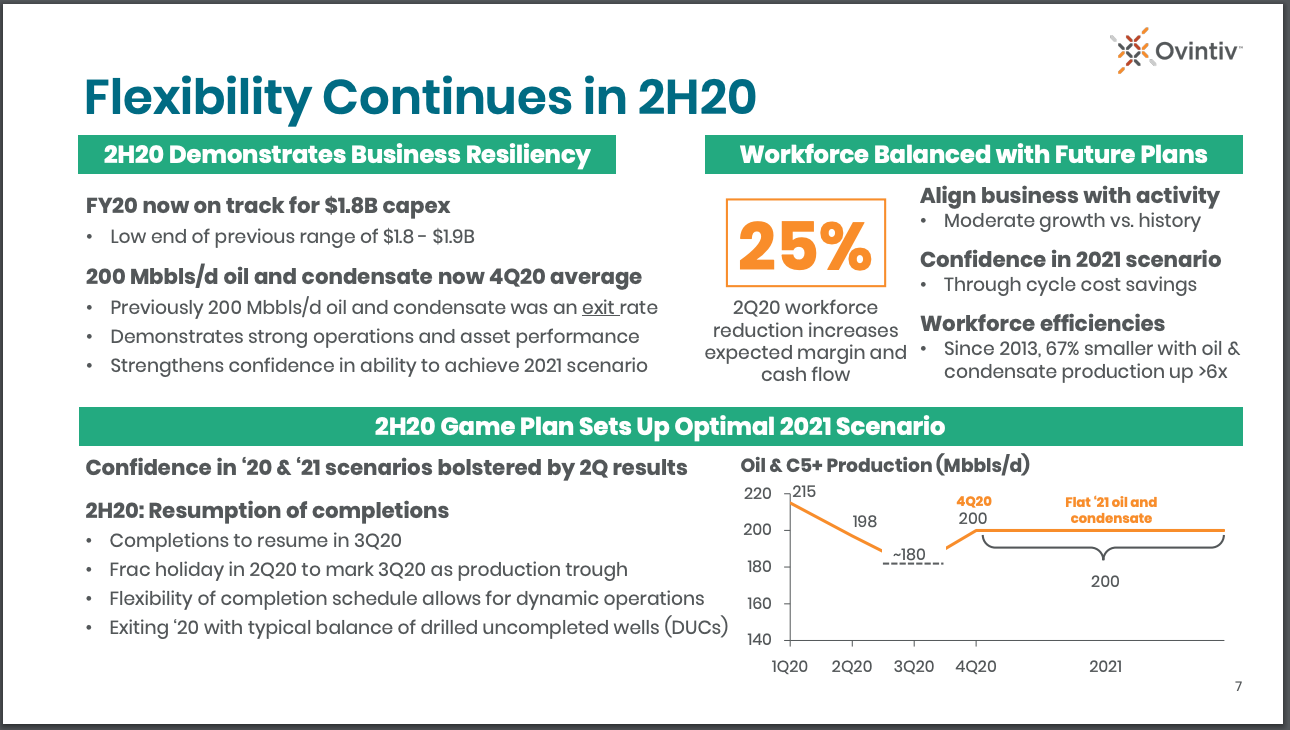

Slide 7:

Firing people saves us money and makes the remaining employees more miserable! That’s how you know you’re resilient. And saying confidence for the third time in the slide deck.

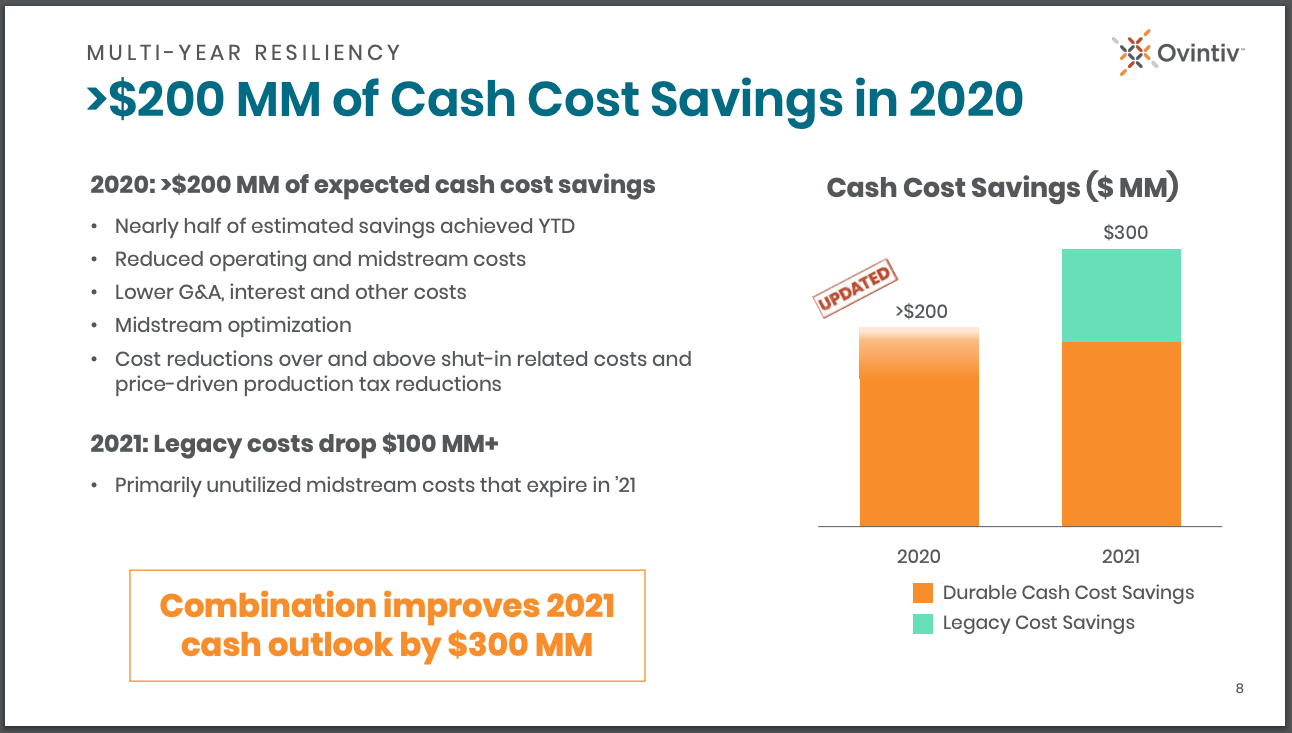

Slide 8:

Nearly half of the estimated annual savings achieved at the end of month 7. We’re already behind! In other news, OVV is now optimizing midstream because there aren’t any more cubes to optimize. Also, how is cash cost savings not durable?

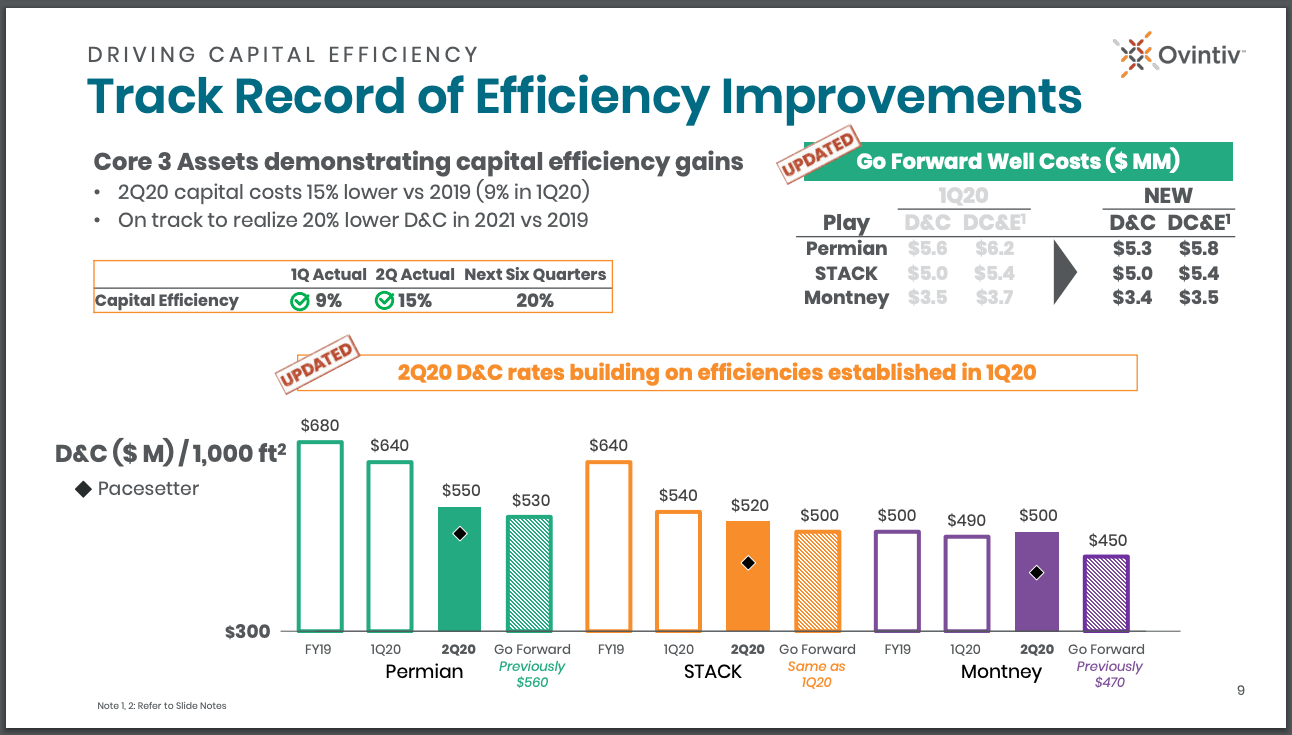

Slide 9:

The ‘sustainable’ part of the OVV business story, lower D+C costs and increased efficiencies. Also, shout out to the one pacesetter well in every basin that makes life hell for the drilling managers trying to drop costs for the next three years.

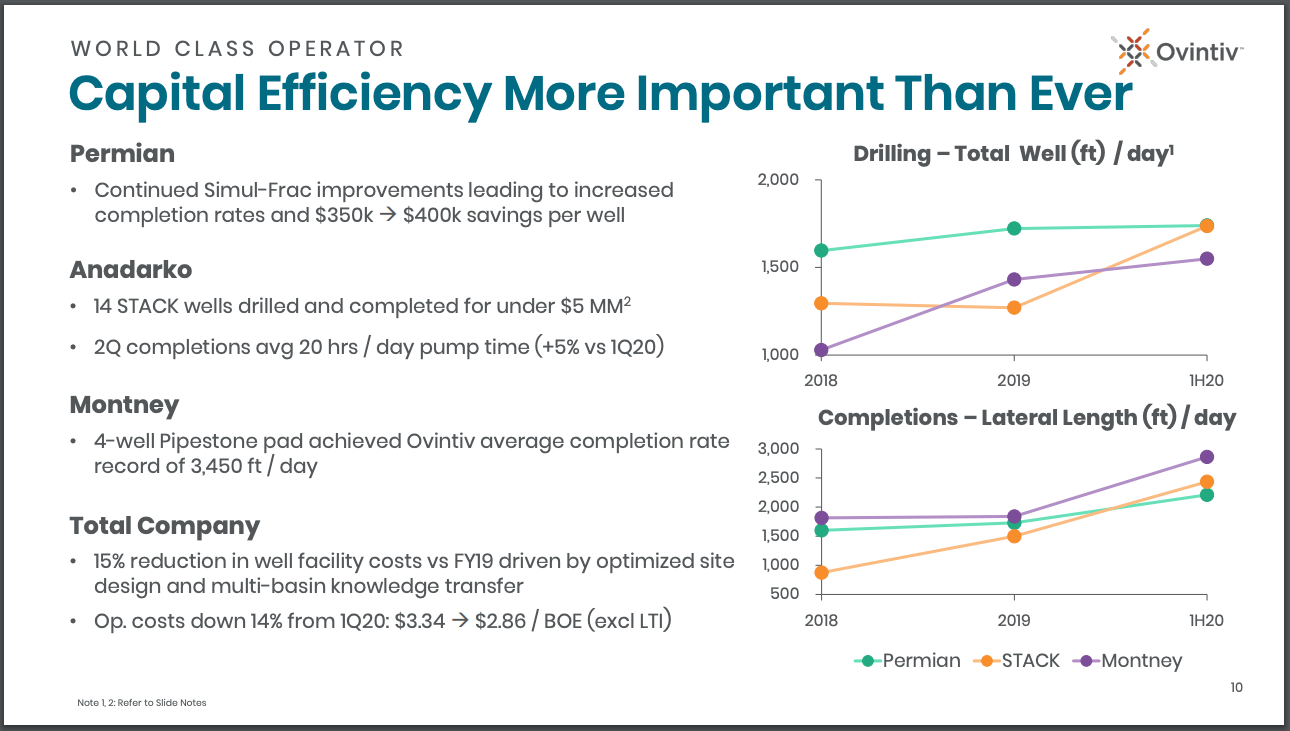

Slide 10:

Just a reminder that OVV actually completed 14 STACK wells in Q2, if you’re wondering where the Q1 2021 impairment charges are coming from.

Slide 11:

The narratives match the background photo. During a time when many view the sun is setting on the industry, it’s actually setting just on OVV.

Slide 12:

Ah, the grand finale. OVV reminding you that they’re:

- Multi basin

- Poorly responding to getting punched in the face by Covid-19

- Have industry-leading efficiency in incinerating capital (you’ll note “cube” isn’t in the deck)

- Size and scale includes a photo of Doug’s bicep

- Unique combination of capital flexibility still completing STACK wells in a poor pricing environment

- The corporate culture is “one” because that’s how many employees care

- And finally: a team of talented and committed industry professionals until they all get laid off.

That’s it for today’s analysis of OVV’s IR decks, please stay tuned for future observations from other #premier oil and gas companies.

Take care and stay fresh,

~Doug